As political uncertainty continues to ratchet higher in Westminster, amid reports that a formal leadership challenge against PM Starmer could be triggered as soon as Thursday, UK assets, in particular Gilts, are facing a trifecta of significant issues.

Firstly, though, some context. Before the ‘starting gun’ has even been fired on a potential leadership contest, we have seen the market becoming very jittery indeed. Cable, for instance, has dipped to 2-week lows beneath the $1.35 mark, EUR/GBP has rallied to its best levels since mid-April, while both 10- and 30-year Gilt yields have printed fresh YTD highs.

_10_2026-05-13_13-39-01.jpg?format=pjpg&auto=webp&width=1536&quality=75&branch=main)

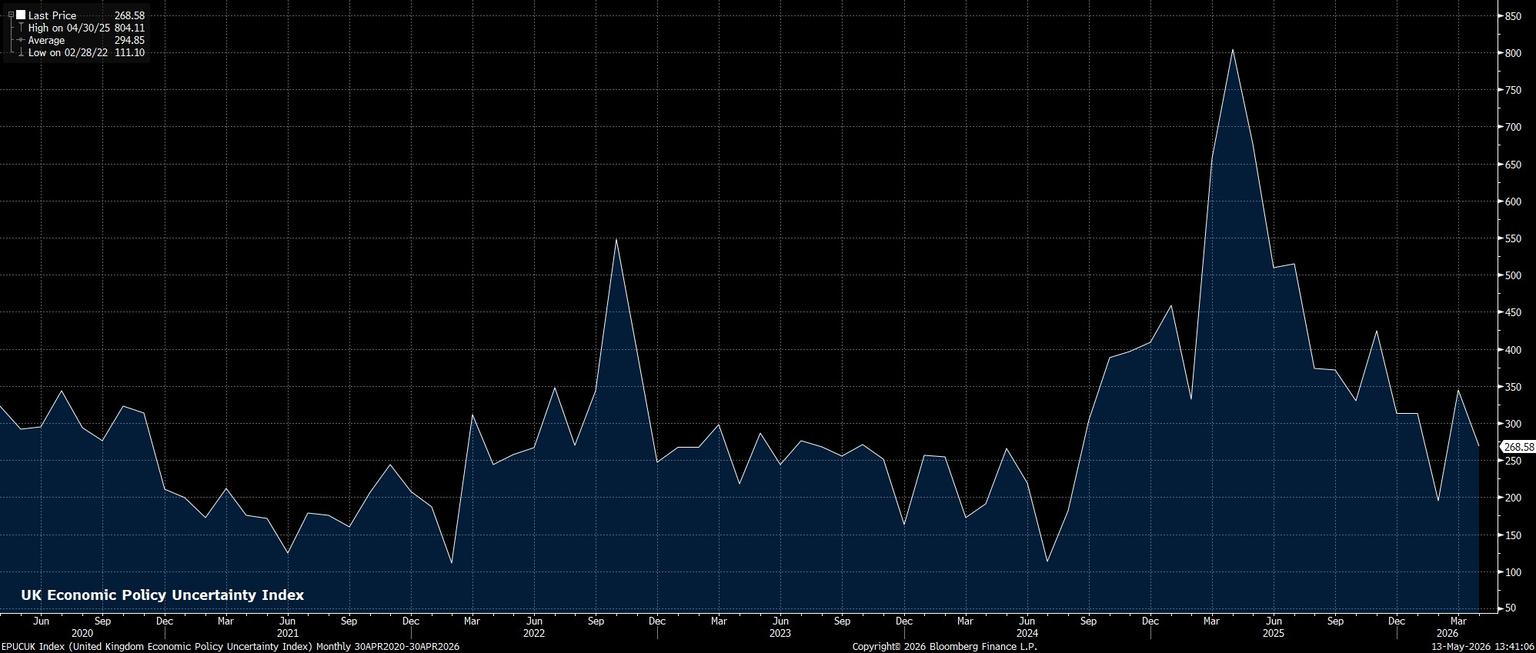

Pricing An Uncertainty Premium

With that said, when considering the market implications of UK political developments, there are three chief concerns that market participants possess.

Firstly, there is the general degree of uncertainty. Given that markets, no matter the country or the asset class, work akin to a forward-looking discounting mechanism, when the path forwards is difficult, or impossible, to price, market participants are forced to associate a higher risk premium, almost always in the form of a lower price, with the asset in question.

This is exactly the dynamic that is currently playing out with the quid, Gilts, and London-listed equities, given that it is unclear who the PM will be, and what their economic policy stance will look like, by the end of the week, let alone in a year or two’s time.

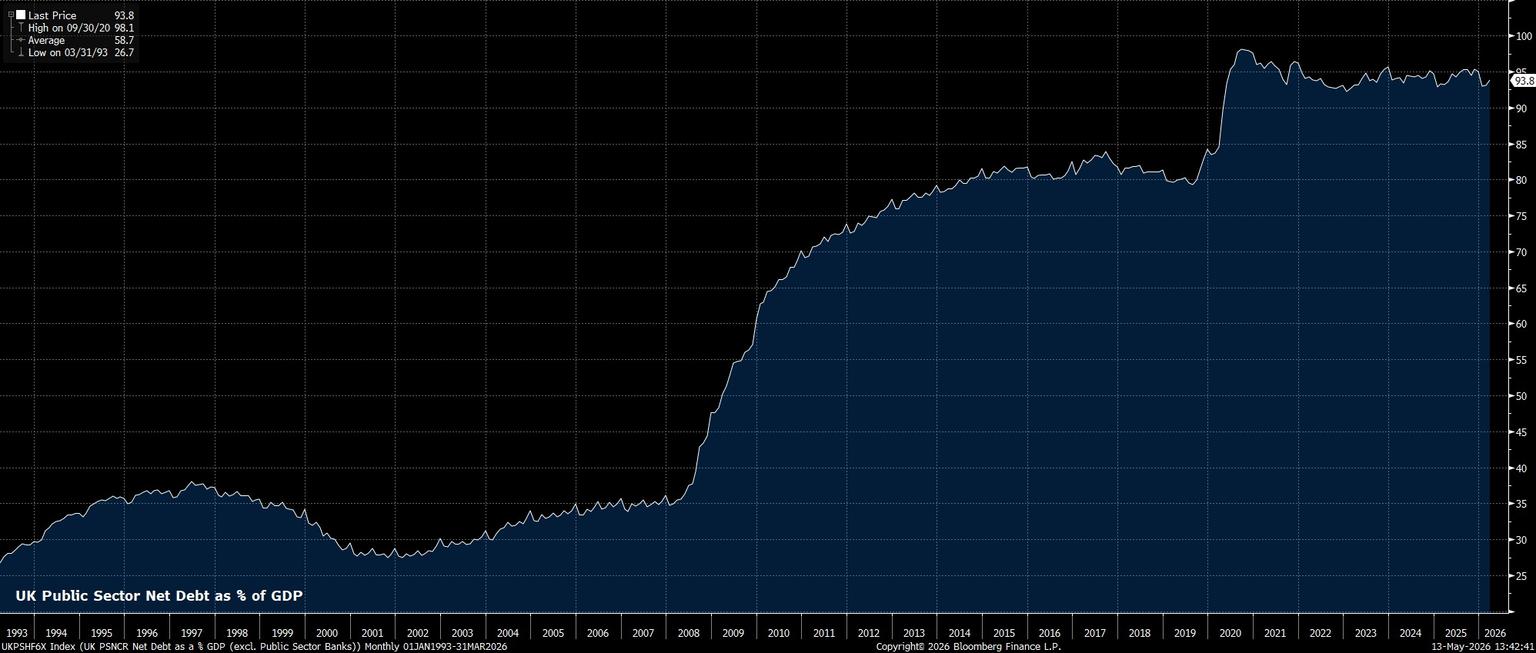

Deficit Set To Widen Further

Secondly, given that a Labour leadership challenge now seems highly likely, and that PM Starmer winning such a contest is implausible, investors are also being forced to reckon with the probability that whoever wins such a contest will adopt a considerably looser fiscal approach.

The rationale here is that, with any candidate needing to obtain the support of Labour members in order to obtain the ‘top job’, the candidates in question will likely need to run on a much more left-wing, fiscally profligate platform, in order to appeal to those very members. Were such policies – likely entailing considerably higher public spending, on areas such as welfare that the market would deem as unproductive – to be delivered, this would threaten the fiscal consolidation that the UK is currently undergoing. In turn, this higher level of spending would lead to more borrowing, and a wider budget deficit, all factors that the market would take a very dim view of.

A Worsening Inflation Problem

Thirdly, this further loosening of the fiscal stance, if it were to come to fruition, would in all likelihood exacerbate the UK’s apparent problem with persistent price pressures.

Excluding the pandemic period, both headline and core CPI have been running consistently north of the Bank of England’s 2% inflation aim for the bulk of the last decade. Although there have been a series of negative supply shocks over this period, with the ongoing Middle East conflict the latest in that sequence, it is becoming increasingly difficult to deny that the UK has an inflation problem. A looser fiscal stance could bring with it further upside inflation risks, while also likely extending the timeline for inflation to return to the Bank’s target. Clearly, this is a further negative catalyst for Gilts, as participants demand a higher yield to compensate for expected higher inflation, but that increased carry is unlikely to be GBP bullish, not least considering that tighter financial conditions will be yet another growth headwind for the economy to grapple with.

Market Implications

All told, there are a couple of implications here.

Firstly, no matter how much senior politicians want to express their distaste with being ‘in hock’ to the bond market, participants will remain sceptical of the UK’s economic backdrop, and continue to discount a greater risk premium in UK assets, unless and until the fiscal position is consolidated. Tearing up the ‘fiscal rules’, and shifting to an even larger ‘tax and spend’ approach would encourage the market to take an even more downbeat view of proceedings.

Secondly, risks to UK assets, be they Gilts, or the GBP, continue to tilt firmly to the downside in the near-term, taking into account the cloudy political backdrop, heightened risk of looser fiscal policy, and downside risks to economic activity at large. The late-March lows in cable, just shy of the 1.32 figure, seem likely to be re-tested as the political melodrama in Westminster drags on.

_2026-05-13_13-43-33.jpg?format=pjpg&auto=webp&width=1536&quality=75&branch=main)